Good morning!

The numbers involved in yesterday’s SpaceX IPO filing were staggering. But with OpenAI and Anthropic expected to follow suit, the broader impact of these new listings could be more complex than we’re used to.

The FT leads with a story this morning highlighting how new “fast entry” rules on the Nasdaq exchange will allow these tightly-held new listings (with small free floats) to gain index membership within weeks of listing. This could force passive funds to sell billions of dollars of Magnificent 7 stocks in order to buy shares in the new entrants, regardless of price - triggering a round of volatility…

In macro news, Iran and the US appear slightly closer to a deal after the US submitted new peace proposals, but demands for Iran to hand over its uranium stockpile appear to be a sticking point. The US is also understandably opposed to Iran’s ongoing efforts to levy tolls on Hormuz traffic.

Meanwhile, concern about the impact of disruption to energy and fertilizer supplies continues to grow, with International Energy Agency chief Faith Birol warning in a speech in London that oil markets could enter a “red zone” by July or August.

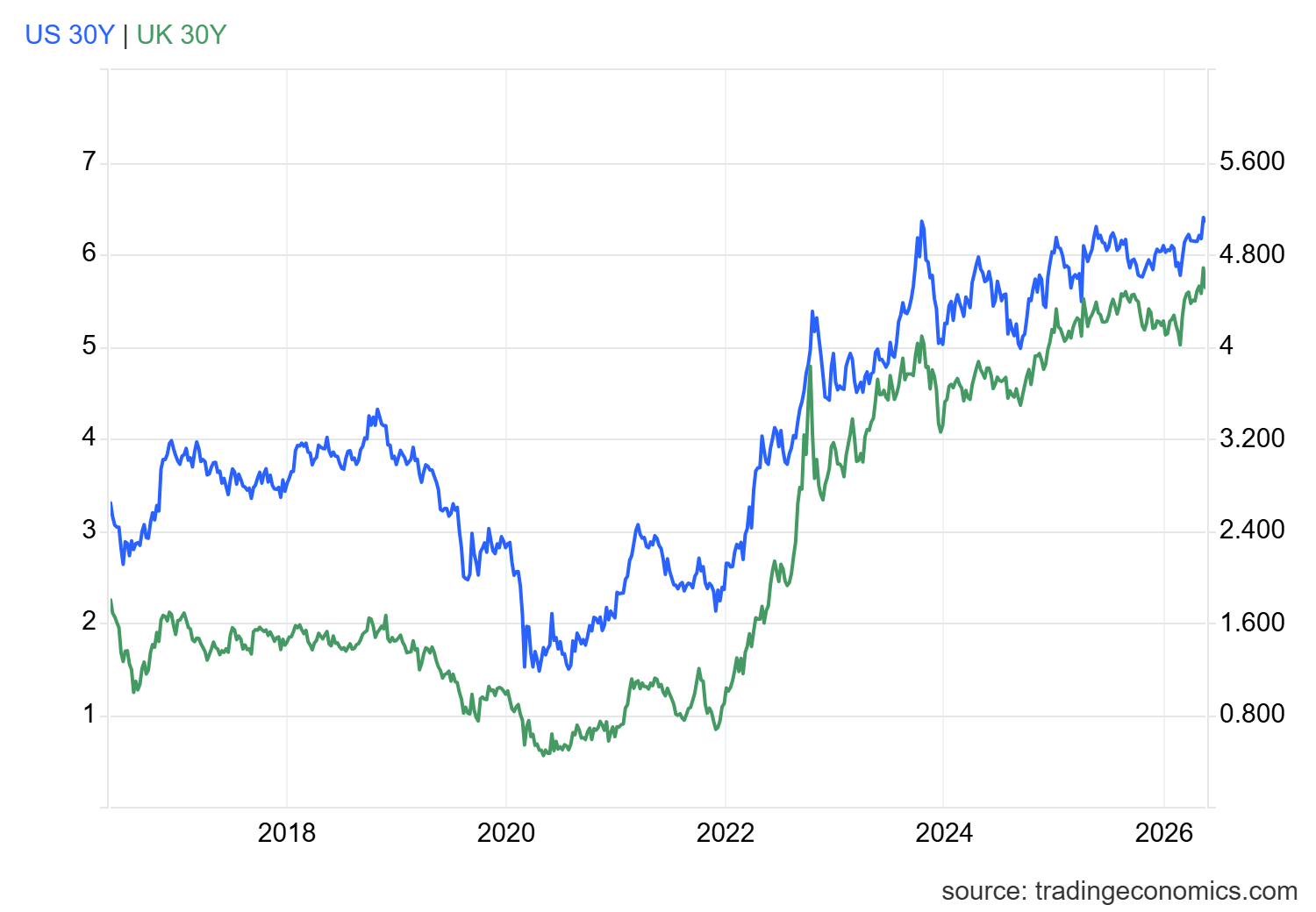

Bond investors – traditionally seen as the smart money – are also concerned about another major spike in inflation, less than five years after the Ukraine war triggered a previous bout. Long-term borrowing costs for major developed markets continue to rise:

However, the saying goes that bull markets climb a wall of worry. Animal spirits certainly seem to remain strong at the moment, with the big US indices continuing to trade at record highs:

Major markets are also expected to open higher this morning:

FTSE 100 expected to open up 0.4%

S&P 500 expected to open up 0.4%

Nasdaq 100 expected to open up 0.5%

Brent Crude is up 1.9% at $102 a barrel

Gold is up slightly at $4,537/oz

That's all for today. Thank you for all your comments this week, I hope you enjoy the long weekend. We'll be back on Tuesday morning!

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Games Workshop (LON:GAW) (£6.3bn | SR67) | Core revenue for the year ending 31 May 2026 is expected to be not less than £625m, with licensing revenue of at least £30m and group pre-tax profit of not less than £265m (FY25: £262.8m). | GREEN = (Roland) Growth in the core business slowed somewhat during the second half, while full-year licensing revenue failed to match the very strong performance in the prior year. However, both of these trends appear to be in line with both expectations and historical trading patterns. I don’t see any serious concerns. This remains an exceptional business, with a differentiated business model, strong IP and continuing growth. I’m going to retain our positive view. | |

Inchcape (LON:INCH) (£2.9bn | SR84) | Inchape has acquired the official distributor of Mercedes-Benz cars and Daimler Trucks and Buses in Bulgaria. This will add to the group’s existing c.13% share in passenger vehicles and 6% share in LCVs in Bulgaria. Silver Star had revenue of c.£240m last year. | ||

Softcat (LON:SCT) (£2.8bn | SR77) | Good performance in Q3, with double-digit growth in gross profit and underlying operating profit. Corporate and AI-related demand remains strong. Now expect mid-teens growth in underlying operating profit, from high-single-digit previously. | AMBER/GREEN = (Roland) Today’s upgrade is the second this year and highlights continued strong momentum from demand for new AI infrastructure. The shares don’t look particularly cheap but I think the business should keep performing well while demand remains strong. At some point the music will stop, or at least change, but how soon that will be is impossible for me to gauge. For now, I think a moderately positive view is fair, reflecting the stock’s High Flyer styling. | |

| Bodycote (LON:BOY) (£1.20bn | SR87) | Response to media speculation (issued 22/5 pm) | Bodycote confirms that it has received a conditional takeover proposal for Apollo Global Management comprising a cash offer of 885p per share + the 2025 final dividend of 16.1p. This follows "a number of previous proposals" from Apollo. The two companies are in discussions. | PINK |

Genuit (LON:GEN) (£659m | SR63) | Year-to-date revenue down 0.4% to £198.5m (-8.7% LFL). Middle East and UK market conditions have affected sales and resulted in cost inflation. Genuit has implemented double-digit price increases. 2026 underlying operating profit now expected to be at the lower end of market forecasts. | BLACK | |

Workspace (LON:WKP) (£648m | SR43) | Saba Capital (21% holder) has submitted a revised requisition notice that now calls for the removal of all six of the company’s non-execs and the appointment of six new directors in their place. | ||

Metals Exploration (LON:MTL) (£426m | SR77) | Gold production down 22.2% to 65,287oz, with sales up 9.1% to $208m and operating profit up 15% to $61.6m. La India development 33% complete at year end, slightly ahead of schedule and within budget. | ||

Enquest (LON:ENQ) (£360m | SR95) | Year-to-date production has averaged 41.5 kboe/d, within 41-45 kboe/d guidance range. Six-well drilling programme at Magnus is now underway. | ||

Altyngold (LON:ALTN) (£286m | SR94) | Gold sales rose by 29% to 11,532oz, resulting in a 122% increase in revenue to $56.3m. Remains confident in the outlook for the remainder of 2026. | ||

Helical (LON:HLCL) (£233m | SR42) | EPRA earnings per share up 105% to 4.5p, reflecting greater development profits. Net rental income down 21% to £15.4m. EPRA NTAV of 351p (FY25: 348p), with LTV of 36.5% (FY25: 20.9%). Confident outlook citing constrained supply of good quality office space in London. | ||

Fonix (LON:FNX) (£157m | SR65) | Company will undertake buyback of 1.25m shares today at 159p, in coordination with the sale of the same number of shares by Richard Thompson, a member of the Concert Party controlling 33% of Fonix shares. | ||

Mobico (LON:MCG) (£130m | SR55) | On 12 May 2026, WMATA issued a notification of termination to Mobico’s US subsidiary to cease operating paratransit services. This follows a lawsuit for breach of contract discussed in Mobico’s 2025 results. | ||

Gemfields (LON:GEM) (£70m | SR28) | Auction revenue of $26.8m, 36/37 lots were sold, totalling 183,385 carats. Average realised price of USD 146.08 per carat. | ||

Creo Medical (LON:CREO) (£47m | SR49) | FY25 Final Results, Proposed Sale of 49% Interest in Creo Medical SL & Placing to raise approximately £5.5m | Revenue +50% to £6m, with underlying operating loss reduced by 38.5% to £13.7m. Now expects revenue growth of 50-60% in 2026 (previously 40-60%). Announces a placing to raise £5.5m at 15p per share. Also intends to sell remaining 49% share of Creo Medical Europe, following a 51% sale last year. Sale said to be priced in line with year-end carrying value. | |

Zenith Energy (LON:ZEN) (£32m | SR44) | Agreed terms for the sale of the ZEN-260 for total gross consideration of approximately US$4.3 million to a company operating in the oil and gas sector in the Philippines. | ||

Headlam (LON:HEAD) (£30m | SR31) | Completed three previously announced disposals, generating net proceeds of c.£15.3m. Continues to evaluate the potential sale and leaseback of the Coleshill property. | RED = (Roland) [no section below] I’m not sure why the share price has reacted so strongly to today’s update, as it doesn’t contain any new information. Details of these property sales were confirmed in an update on 20 May, which today’s update repeats almost verbatim. These disposals were also flagged in March’s full-year results. The main point I would take from today’s update is that the cash from these sales is being used to “invest in working capital” and improve liquidity. To me, this sounds like cash from the sale of long-term assets is being used to keep the lights on and fund day-to-day operations. I might be more positive if the proceeds were explicitly being used to repay long-term debt. My concern is that if the business remains loss-making at an operating level, its runway for survival could be limited. I note forecasts show an adjusted net loss in 2026 and 2027 – not ideal given material debt levels. I’m going to retain our negative view today. As I discussed in more detail recently, I think the equity looks risky here. | |

FIH (LON:FIH) (£28m | SR62) | Sale and leaseback of Momart warehouse in Leyton completed in Sept 25, generating a pre-tax return of £11.8m. Sale of Portsmouth Harbour Ferry Company completed on 28 Feb 26 delivering net proceeds of £10.7m. Transaction costs included bonus payments of £478k and £239k for the CEO and CFO, respectively, for completing these divestments. Shareholders will receive a 40p special dividend on 14 July 2026 (ex-divi 4 June 2026). | No view (Roland) [no section below] Without passing any comment, I would like to highlight that the CEO and CFO effectively appear to have shared a 3% commission on the sale of these assets through their bonus payments. | |

Hercules (LON:HERC) (£28m | SR n/a) | Final Results and H1 Trading Update & Restoration to Trading | FY25 revenue +19% to £121m, ahead of expectations. Underlying EPS +36.6% to 4.74p (y/e 30 Sept 25). Qualified audit opinion. H1 FY26 revenue +8.4% to £59.2m. No FY26 guidance or house broker forecasts. Shares restored to trading today. | AMBER/RED ↓ (Roland) These final results reveal that Hercules suffered accounting irregularities relating to certain suppliers last year, which the auditors were unable to resolve. There is also no guidance for FY26 and broker Singer Capital has opted not to provide FY26 forecasts, despite the year being nearly two-thirds complete. The main uncertainty seems to relate to the potential impact of delays to infrastructure projects. There is too much uncertainty here for me to maintain a positive or even neutral view. The interim results are due in June and will hopefully provide some clarity on the state of the business and the full-year outlook. Until then, I’ve opted to move our view down by two notches to be moderately negative. |

Checkit (LON:CKT) (£27m | SR40) | “Since the commencement of the Formal Sale Process, the Company has received credible interest from potential acquirers. Discussions with these parties are ongoing and further announcements will be made as and when appropriate.” | ||

Tekcapital (LON:TEK) (£16m | SR56) | Exec Chairman Clifford Gross has launched a new company to commercialise IP in the field of geothermal-powered data centres. Tekcapital will gain a 51% equity interest for no cash consideration, with Gross retaining the remaining 49% interest. | ||

Zinc Media (LON:ZIN) (£14m | SR16) | Agreed to acquire William Martin Qatar LLC, an event production business, for an initial net consideration of £0.4m, to be funded with shares. In 2025, WMP Qatar generated a pre-tax profit of £0.3m and had net assets of £0.5m. | ||

Rua Life Sciences (LON:RUA) (£13m | SR42) | Expects revenue +6% to £2.8m, with gross margin of 75%. H1 EBITDA expected to be at break even. | ||

Sound Energy (LON:SOU) (£11m | SR15) | “Significant progress has been made in advancing the sustainability of the Company through the transformational transaction with Managem in 2024. Revenue generation from mLNG is expected in the near future.” |

Roland's Section

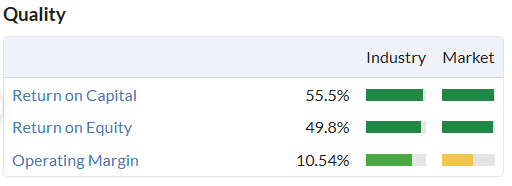

Games Workshop (LON:GAW)

Up 4% at 19,830p (£6.5bn) - Full Year Trading Update - Roland - GREEN =

This morning’s update from Games Workshop is fabulously concise. My summary comment in the table above is almost the entire RNS!

Here is the fully copy:

Games Workshop, the maker of Warhammer, is pleased to announce that for the 52 weeks ending 31 May 2026, we estimate the Group's core revenue to be not less than £625 million (2024/25: £565.0 million) and licensing revenue of not less than £30 million (2024/25: £52.5 million). The Group's profit before taxation ("PBT") is estimated to be not less than £265 million (2024/25: £262.8 million).

We intend to publish our 2026 Annual Report for the 52 weeks ended 31 May 2026 on the 28 July 2026.

What should investors take from this update?

Today’s update covers the year to 31 May 2026 and looks to be in line with expectations:

Total revenue up 6% to at least £655m (FY25: £618m)

Total pre-tax profit up 0.8% to at least £265m (FY25: £262.8m)

These figures tell us the group’s pre-tax profit margin fell from 42.5% to 40.5% last year. My sums suggest this reflects the lower contribution from licensing revenue rather than any weakness in core margins (licensing revenue carries a margin of nearly 100%):

Core revenue (figures and game products) up 10.6% to £625m

Licensing revenue (video games and TV/film) down 43% to £30m

However, comparing today’s figures with the half-year results suggests growth in the core business slowed during the second half of the year, with core revenue falling below H1 levels:

H1 core revenue: £316.1m (+17.3% vs H1 FY25)

H2 core revenue: £309.9m (+4.5% vs H2 FY25)

This isn’t unprecedented for this business and is perhaps not that surprising, given the macro backdrop during the second half (Nov-May).

The company’s decision to provide no commentary on trading in today’s update means we’re left guessing, but given that consensus forecasts suggested full-year revenue of £643m, today’s figures do not seem to suggest any surprises.

Outlook: Games Workshop doesn’t provide any forward guidance and we don’t have access to any broker notes for the business. However, the limited market reaction to today’s update suggests to me that market forecasts for FY27 are likely to remain largely unchanged, as they have been since November:

Roland’s view

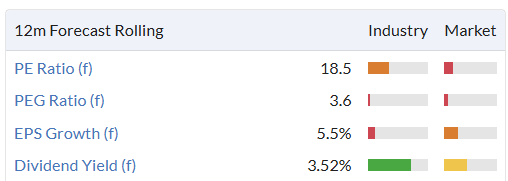

As usual, Games Workshop shares do not look obviously cheap:

But the quality of this business is exceptional, as is its long-term growth record. This justifies a premium valuation, in my view.

While licensing revenue was weaker this year, a more “challenging” environment was flagged up in the H1 results and appears to have been expected. The group’s live action venture with Amazon MGM Studios continues to progress, as do various video game partnerships.

It is the nature of these things to take several years, and while we wish we could tie down a release the way we can with our core business, the reality is that, as with any licensing deal, delivery is not in our control. We leave it to our partners to manage their own businesses.

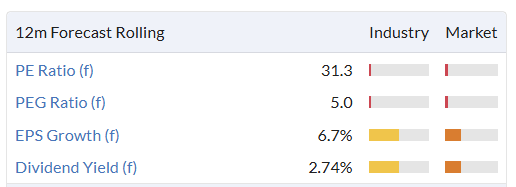

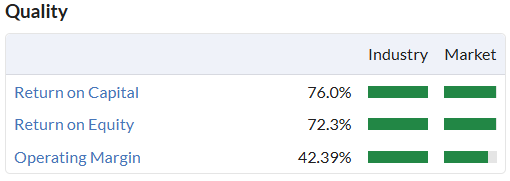

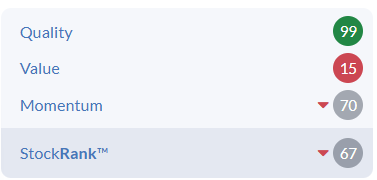

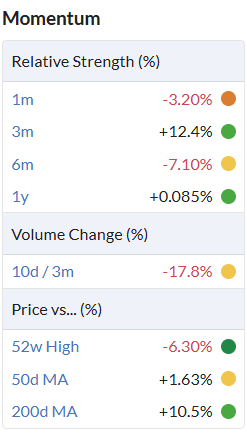

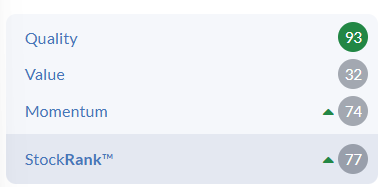

The StockRanks rightly flag Games Workshop as a High Flyer…

The low ValueRank is unsurprising, but perhaps it's worth noting that momentum has weakened recently:

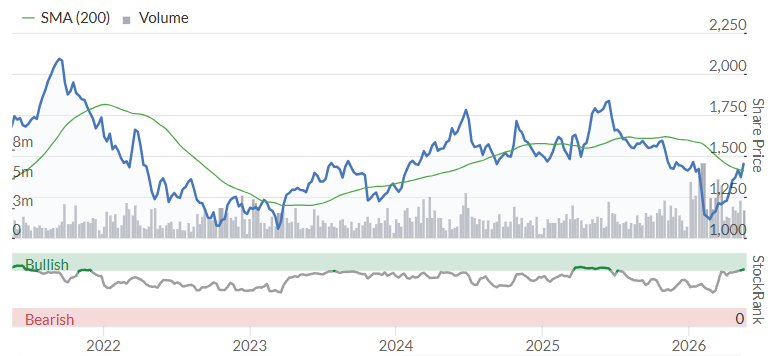

Despite this, the medium-term uptrend on the chart still looks fairly healthy to me:

We were positive on Games Workshop in January and I don’t think the story has changed since then, so I’m going to keep our view at GREEN today.

Softcat (LON:SCT)

Up 11% at 1,600p (£3.1bn) - Q3 Trading Update - Roland - AMBER/GREEN =

Softcat shares remain below historic highs, but today’s upgrade to full-year expectations suggests the business is continuing to perform well and benefit from AI-related data centre demand.

The AI boom has led to massive growth in hardware revenue for value-added resellers such as Softcat, as they supply the high value, high volume kit required to build out new computing infrastructure.

Softcat’s half-year results showed gross invoiced income up 33%, with hardware sales up 79%.

Today’s third-quarter update covers the three months to 30 April 2026. It’s brief and lacks any specific numbers, but suggests to me that the underlying trends haven’t changed.

Q3 Trading: key points

“... strong double-digit year-on-year growth in gross profit and underlying operating profit”

“Growth remains broad-based with particular strength in corporate, supported by customer demand for AI-enabled infrastructure and continued pull forward of some orders due to memory shortages.”

Outlook

Looking further ahead, the Board is encouraged by the momentum in the business and prospects for continued market share gains, while recognising the uncertainty caused by the ongoing memory shortages and macroeconomic environment.

As a result of the strong performance so far this year, guidance for profit growth has been upgraded:

New FY26 guidance: “mid-teens operating profit growth” up from “high single digit previously”

I don’t have access to broker forecasts today, but a c.15% increase in underlying operating profit is likely to drop through to at least a c.10% increase in adjusted earnings per share.

This morning’s share price gain seems to support that view. Applying a 10% increase to previous consensus of 75p per share suggests a new FY26E EPS estimate of perhaps 83p. That would leave the stock’s forward P/E of 19 largely unchanged.

Today’s upgrade is the second this year from Softcat, highlighting the strong momentum in this market at the moment. However, limited visibility means forecasts for next year’s earnings have remained somewhat flatter:

Roland’s view

I have both an interest in and a bias towards this sector, as Softcat’s larger peer Computacenter (disc: I hold) is one of my largest personal holdings.

While these value-added resellers are low-margin businesses and can be seen as middlemen, they have evolved over the last 20 years to be an essential conduit between suppliers and end users. Even the largest hyperscalers source at least some of their IT requirements through resellers, who are able to coordinate, supply and implement large and complex solutions:

Our uniquely broad offering brings together specialisms from the datacentre to the edge, through the network, security, data and automation layers, and across hardware, software and services, spanning the design, implementation, management, support and optimisation of new solutions.

From a financial perspective, companies such as Softcat are able to generate attractive returns on capital by benefiting from favourable supplier credit terms on high volumes of product. Cash generation is also generally very strong.

Softcat and its peers are undoubtedly benefiting from the boom in AI infrastructure. But there’s obviously a potential flipside to this – at some point, spending will probably moderate. Predicting when that happens is beyond my paygrade, but personally I may choose to top slice my exposure to this sector at some point in the future in order to lock in profits and hedge against any slowdown risk.

I think this situation is nicely reflected in Softcat’s High Flyer status and high-VM StockRank:

For this mix of reasons, I am leaving my previous AMBER/GREEN view unchanged today.

Hercules (LON:HERC)

Up 2.6% at 35p (£29m) - FY25 Results and H1 FY26 Trading Update - Roland - AMBER/RED ↓

Hercules shares have returned from suspension and today following the publication of the company’s long-delayed results for the year ended 30 September 2025. That’s right, it’s taken nearly eight months for this small cap to issue its annual results – almost two months longer than the generous AIM market limit of six months.

Why the delay?

In March, the company said the delay was due to “the consolidation of acquisitions and further work needed to review certain sub-contractor contracts”.

Today we learn that the delay was caused by audit investigations into irregularities in Hercules’ accounting records – essentially, the company did not have sufficient records to provide an audit trail for payments to some training and consultancy providers.

Here’s what the auditors had to say about this issue:

During our audit work, we were approached by an individual who raised concerns relating to payments made to a limited number of training and consultancy services providers. Following investigations by management, certain irregularities were identified in respect of a number of related transactions within the group and parent company.

These transactions have been categorised within the Group's accounting records as being in respect of training and consultancy costs. However, we were:

· unable to confirm that sufficient appropriate supplier onboarding processes had been followed

· unable to confirm whether the companies were bona fide suppliers

· unable to confirm that related appropriate training or consultancy services had been provided or that amounts paid in respect thereof properly related to the provision of training or other expenditure made for the benefit of the business

This has resulted in a qualified audit opinion for the FY25 results and what sounds like a disagreement between management and the auditors over whether to pursue investigations to an ultimate conclusion:

We sought to obtain further evidence but were unable to do so because management decided against concluding further investigative efforts into the transactions prior to the signing of the financial statements and thus imposed a limitation of our scope. We requested that the Board remove management's limitation, which they did not.

The short version seems to be that the Board decided the time required and low likelihood of success of further investigations meant they were not worthwhile. The shares were suspended and the Board was keen to publish the company’s FY25 results so that the suspension could be lifted.

The end result is that the questions raised during the audit have not been fully addressed.

Hercules makes the following statement about this in today’s results:

… the Board recognises that some gaps in audit evidence remain and that, in some cases, the audit trail is incomplete.

Remediation work to bring the company’s controls up to standard is still ongoing:

However, the specialist accounting and legal workstreams, and the detailed remediation work commissioned across the Company's systems, processes, and controls, have provided the Board with confidence the relevant systems and processes have been largely remediated and expects the remaining remediation work to be completed by 30 September 2026.

The auditors have this to say (my emphasis):

We have concluded that this matter is material to the Group Financial Statements. In respect alone of this matter, we were unable to determine whether any adjustments to amounts or disclosures in the financial statements are necessary, or whether there have been any breaches of applicable laws or regulations.

What should shareholders think? There are clearly two ways to interpret this issue.

The charitable view is that the company has suffered growing pains during a period of rapid expansion through acquisitions and organic growth. In essence, accounting controls and processes have not kept pace with the growing scale of the business, which has seen revenue double since 2022.

A less charitable view might be that the lack of an audit trail could have been intentional and that shareholders may have been disadvantaged in some way. I should emphasize that I am not suggesting any wrongdoing has taken place. The growing pains version of events seems quite plausible given the rapid expansion of the business since its flotation.

Individual investors will have to form their own view, based on the information provided today.

Let’s move on to take a look at the FY25 results and today’s half-year trading update.

FY25 results

I am not going to spend much time on these figures as they relate to a trading period that ended nearly eight months ago.

Here are the headline figures for last year:

Revenue up 19% to £121.2m, ahead of expectations

Underlying pre-tax profit up 53.8% to £4.0m

Reported pre-tax profit down 59% to £0.9m

Underlying earnings per share up 36.6% to 4.74p

Net debt (exc leases): £4.9m (FY24: £0.9m)

Cash generation: excluding c.£12m of acquisition spending, I estimate FY25 free cash flow was £4.3m from continuing operations. This maps quite nicely onto the group’s adjusted profit figures and does suggest a positive underlying performance.

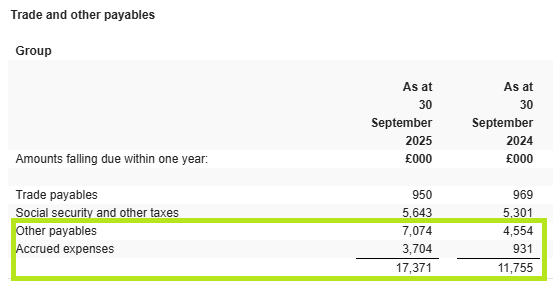

One caveat to this is that outstanding payables rose sharply last year, climbing 48% (+£5.6m) to £17.4m. This far exceeded the 18.5% rise in cost of sales to £103.0m and arguably accounts for all of my underlying free cash flow estimate.

Checking the footnotes suggest this increase in money owed to creditors was primarily down to increases in “other payables” and accrued expenses – goods or expenses that have been supplied but not yet billed for:

I’m not sure what’s included in these two categories; some of the changes may relate to acquisitions and a changing business mix during the year. But I wonder if Hercules might also be finding ways to stretch out payments as long as possible.

On a related note, I see that the company took a three-year £6m loan last year from Wasdell Holdings, a business owned by one of Hercules’ non-executive directors. The interest rate of 8% seems reasonable, but I think it might have been more reassuring to see that a mainstream bank was willing to lend to the business.

Divisional Trading

Labour Supply: during the year, Hercules made the “successful acquisition of Advantage NRG”, providing entry into the Power and Energy sector.

The number of labour clients supplied rose to 65 (FY24: c.40)

Operatives deployed by Labour Supply rose by 7% to 1,230

Construction Services: the acquisition of Quality Transport Training “increased capacity of the Hercules Academy”.

Civil Projects won “significant levels of repeat work” for key delivery partners in the water sector

The Construction Academy has trained more than 2,000 individuals since opening in 2024.

Half Year Trading Update

This is brief – the main points are:

H1 revenue rose by 8.4% to £59.2m

Civil Projects division has benefitted from spending related to the AMP8 (water) investment cycle

The Labour Supply business has been impacted by delays to some infrastructure projects.

Management also notes that both Labour Supply generally and the recently acquired Advantage NRG business generally have H2-weighted results.

Outlook

Hercules has not provided any guidance for FY26 today. This seems a little disappointing, given that the company's financial year ends on 30 September, so is nearly two-thirds complete.

More worryingly perhaps, the company’s house broker, Singer Capital, has also opted not to provide FY26 forecasts in the updated note published today. Singer's analysts cite uncertainty over project delays as the main reason for the lack of visibility on future financial performance.

With this in mind, I would suggest that the FY26 forecasts shown on the StockReport are likely to be stale and not necessarily very useful.

Roland’s view

Graham gave Hercules the benefit of the doubt and maintained a moderately positive view when we last commented on this business in February.

I can't do that today, given the past, present and future uncertainties highlighted by today’s announcement.

Based on last year’s accounts (which the auditors say may carry some material uncertainty), Hercules shares trade on 7.4x FY25 adjusted earnings. In the normal course of things, I would say a sub-10 P/E would be about right for a low-margin construction contractor.

However, with no fresh forecasts in the market for FY26, I cannot say how that multiple might look for the current year.

Hercules has promised to publish its half-year results (for the six months to 31 March) in June. Hopefully they will be free of accounting uncertainties and provide some meaningful guidance for the current year. Until then, I am going to cut our view by two notches to AMBER/RED.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.